New Income Tax Act, 2025 vs Income Tax Act, 1961: Major Changes Every Taxpayer Must Know

Published on: July 2026

Author: Investax India

Introduction

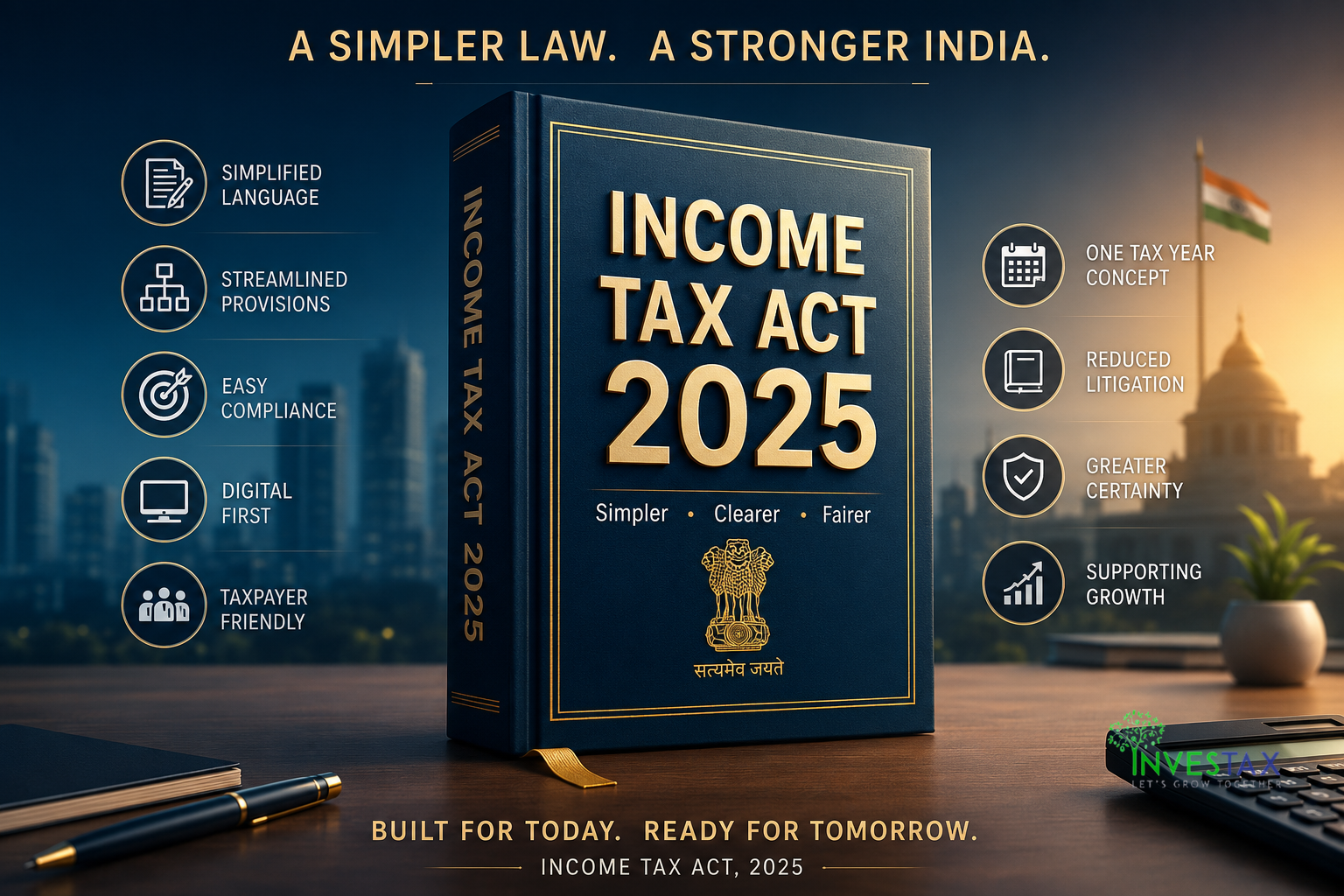

After governing India's direct tax system for more than six decades, the Income Tax Act, 1961 has finally been replaced by the Income Tax Act, 2025, effective from 1 April 2026.

The objective of the new Act is not to increase taxes, but to simplify the tax law, reduce litigation, improve readability, and make tax compliance easier for individuals, businesses, professionals, and tax practitioners. The government has modernized the structure of the law while largely retaining the existing tax policies and rates.

If you're wondering how the new law differs from the old one, this guide explains everything in simple language.

Why Was a New Income Tax Act Needed?

When the Income Tax Act, 1961 was enacted, it contained relatively straightforward provisions. However, over the past 60+ years, numerous amendments, explanations, provisos, judicial interpretations, and new taxation concepts made the Act increasingly difficult to understand.

Some of the major challenges under the old Act included:

-

Complex legal language

-

Hundreds of amendments

-

Excessive cross-referencing

-

Multiple provisos and explanations

-

Confusing section numbering

-

Separate concepts of Previous Year and Assessment Year

The Government therefore introduced the Income Tax Act, 2025 with the objective of creating a simpler, taxpayer-friendly law without substantially changing the tax policy.

Income Tax Act, 1961 vs Income Tax Act, 2025

| Particulars | Income Tax Act, 1961 | Income Tax Act, 2025 |

|---|---|---|

| Effective From | 1 April 1962 | 1 April 2026 |

| Objective | Levy and administration of Income Tax | Simplified and modern tax legislation |

| Language | Technical and legalistic | Plain, reader-friendly language |

| Sections | 819 Sections | 536 Sections |

| Schedules | 14 | 16 |

| Structure | Multiple amendments over decades | Completely reorganized |

| Compliance | Comparatively complex | Easier and digital-friendly |

| Tax Year | Previous Year + Assessment Year | Single Tax Year |

| Cross References | Extensive | Significantly reduced |

| Readability | Moderate | Much easier |

Top 10 Major Differences Between the Old and New Income Tax Acts

1. Introduction of "Tax Year"

Perhaps the biggest conceptual change is the replacement of:

-

Previous Year

-

Assessment Year

with a single term:

Tax Year

This eliminates confusion for taxpayers, students, and professionals.

Old System

Income earned in FY 2025-26

↓

Taxed in AY 2026-27

New System

Income earned during Tax Year 2026-27

↓

Tax calculated in the same Tax Year concept

This simple change makes tax laws easier to understand.

2. Reduction in Number of Sections

One of the most significant structural improvements is the reduction in legislative size.

| Old Act | New Act |

|---|---|

| 819 Sections | 536 Sections |

The reduction was achieved by:

-

Removing obsolete provisions

-

Merging similar provisions

-

Eliminating repetitive explanations

-

Rewriting complex clauses

The result is a shorter and more user-friendly law.

3. Simpler Language

The Income Tax Act, 1961 often required professional interpretation because of lengthy legal drafting.

The new Act:

-

Uses shorter sentences

-

Reduces legal jargon

-

Simplifies definitions

-

Makes provisions easier to understand

This benefits:

-

Salaried employees

-

Small businesses

-

Startups

-

Students

-

Chartered Accountants

-

Tax consultants

4. Better Arrangement of Chapters

Earlier, related provisions were scattered throughout the Act.

The new Act groups similar provisions together, making navigation easier.

Examples include:

-

Salary

-

Business Income

-

Capital Gains

-

TDS

-

Assessment

-

Appeals

-

Penalties

This logical organization improves readability and reduces the time required to locate provisions.

5. Reduced Cross Referencing

The 1961 Act frequently required readers to move between multiple sections.

For example:

Section → Explanation → Proviso → Another Section → Rule

The 2025 Act incorporates many explanations directly into the main provision, reducing unnecessary cross-references.

6. Digital-First Tax Administration

The new legislation recognizes today's digital compliance environment.

It supports:

-

Faceless assessments

-

Electronic notices

-

Online compliance

-

Digital communication

-

Improved e-governance

This aligns tax administration with India's Digital India initiative.

7. Tax Rates Remain Largely Unchanged

Many taxpayers assumed that the new Act would introduce new tax rates.

This is not true.

The Income Tax Act, 2025 primarily changes the structure and drafting of the law. Tax rates continue to be determined through the Finance Act and annual Budget process.

8. Better Compliance for Small Taxpayers

The new Act is designed to reduce dependence on tax professionals for routine compliance by:

-

Simplifying legal language

-

Organizing provisions logically

-

Reducing ambiguity

-

Improving accessibility

The aim is to make compliance less intimidating for individual taxpayers and small businesses.

9. Modern Drafting Style

Instead of long paragraphs with multiple provisos, the new Act uses:

-

Tables

-

Formulas

-

Structured clauses

-

Better formatting

This improves interpretation and minimizes confusion.

10. Easier Interpretation and Reduced Litigation

One of the government's primary goals is to reduce disputes arising from complex drafting.

By simplifying the language and consolidating provisions, the new Act seeks to make tax law more predictable and reduce unnecessary litigation over interpretation.

What Has NOT Changed?

Despite the comprehensive rewrite, several fundamentals remain unchanged:

-

Basic taxation principles

-

Heads of income

-

Residential status concepts

-

Taxability of salary

-

Capital gains framework

-

Business income computation

-

TDS and TCS mechanisms (though reorganized)

-

Annual Budget process for changing tax rates

The legislation is therefore more of a structural modernization than a complete overhaul of tax policy.

Benefits of the New Income Tax Act, 2025

For Individual Taxpayers

✔ Easier understanding of tax provisions

✔ Simplified filing process

✔ Less confusion over legal terminology

For Businesses

✔ Better compliance

✔ Simplified reference to tax provisions

✔ Improved certainty

For Chartered Accountants & Tax Professionals

✔ Better organized legislation

✔ Easier section mapping

✔ Faster research

✔ Reduced interpretational complexity

For Students

The new Act is significantly easier to study due to:

-

Logical arrangement

-

Simpler language

-

Better numbering

-

Reduced duplication

Possible Challenges During Transition

As with any major legislative change, taxpayers and professionals may face some initial challenges:

-

Learning new section numbers

-

Adapting to the "Tax Year" concept

-

Updating tax software

-

Revising educational material

-

Understanding transitional provisions for pending assessments

However, the Income Tax Department has introduced a parallel reading utility to help taxpayers compare provisions of the old and new Acts during the transition.

Frequently Asked Questions (FAQs)

1. Is the Income Tax Act, 1961 completely abolished?

Yes. The Income Tax Act, 2025 replaces the 1961 Act from 1 April 2026, while transitional provisions ensure pending proceedings continue under the old law where applicable.

2. Have income tax rates changed?

No. The new Act mainly simplifies the legislation. Tax rates continue to be governed through the Finance Act.

3. What is the biggest change?

The introduction of the Tax Year concept replacing both Previous Year and Assessment Year.

4. Will taxpayers have to learn new section numbers?

Yes. Most section numbers have changed because of the complete restructuring of the legislation.

5. Is the new law beneficial?

Yes. The new law is expected to improve readability, reduce compliance burden, simplify interpretation, and support a more digital-first tax administration.

Conclusion

The Income Tax Act, 2025 represents the most significant reform in India's direct tax legislation since 1961. While it does not fundamentally change tax rates or introduce new taxes, it modernizes the legal framework by simplifying language, reorganizing provisions, reducing the number of sections, and introducing the single Tax Year concept.

For taxpayers, professionals, and businesses, the transition will require familiarity with the new structure and section numbering. Over time, however, the new Act is expected to make tax compliance more transparent, efficient, and user-friendly.

As India embraces a simplified tax regime, understanding these changes will help taxpayers remain compliant and make informed financial decisions.

Need Professional Tax Assistance?

Whether you're an individual, startup, or business owner, Investax India can help you navigate the new Income Tax Act, 2025 with confidence. From income tax return filing and tax planning to notices, assessments, and business compliance, our experts are here to assist you every step of the way.